Q1 Fertilizer Summary

Volatility & Uncertainty

Affordability and product availability continue to be key concerns.

KEY HIGHLIGHTS

• Geopolitical tensions continue to disrupt fertilizer markets affecting energy costs, freight, raw material availability and pricing.

‣ Iran-Israel-U.S. conflict began 28 Feb

‣ Russia-Ukraine conflict

‣ Supply and energy shocks – oil, natural gas, ammonia, sulphur, urea and processed phosphates

‣ Continued Freight and Insurance Risks

• China export window for fertilizers is rumored to be pushed back to 30 Aug 2026

• Urea: Firm and Volatile. Approximately 45% of global urea production transits through the Strait of Hormuz.

• DAP: Very Firm. Lack of supply options.

• MOP: Stable to Firm.

• Sulphur: 15-20 year highs. Supply constrained.

• Ammonia: Prices over $1000 per ton

UREA

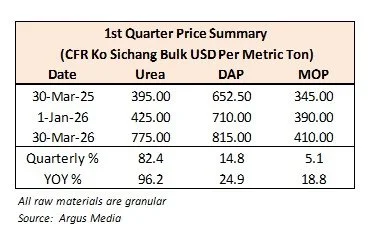

Urea prices increased 82% during Q1 to $775 CFR and were up 96% year-over-year. Local wholesale offers for urea are sparse as importers are having difficulty buying new material.

An India urea tender was awarded at the end of the February at an average price of $510 CFR per ton, up $84 per ton from the previous tender. 2 million tons were tendered for delivery in June. With the inability to secure natural gas, domestic urea production has been under constrained in India putting even more pressure on an already tightly supplied market. China which exported roughly 5m tons in 2025 is currently not exporting urea.

With roughly 50-60% of Urea coming from the Persian Gulf, the Iran conflict has been devasting on supply availability and pricing. The market will remain volatile until there is a conclusion to the conflict.

DAP

DAP prices reversed course increasing 15% in the 1st quarter on supply constraints. Year over year DAP prices were up 25%. Local wholesale prices are over 28,000 Baht in bulk with limited quantity available. Only Russian and Moroccan DAP are being imported consistently.

Sulphur prices continue to climb putting more pressure on phosphate prices. Roughly 50% of global sulphur exports go through the Strait of Hormuz. The conflict has made an already tight market into a severe supply deficit. Additionally, both Russia, one of the world’s largest exporters, and China have banned exports.

China’s export window for DAP is rumoured to have been delayed until 31 Aug 2026 at the earliest. Until the conflict ends, Thailand’s most practical near-term sourcing options are from Russia and Morocco. Egypt, Jordan and the U.S. may also supply spot cargoes. Availability and affordability are major areas of concern as Thailand approaches the main planting season.

MOP

Granular MOP prices have started to trend higher up 5% in the quarter and 19% year over year. Local wholesale prices finished the quarter around 13,500 – 13,900 Baht per metric ton.

Supply was very tight in the first quarter as almost a large portion of production from Laos was exported to China. Israel and Jordan did not export at full capacity because of the conflict and tensions in the Red Sea. Both BPC and Uralchem will regularly bring in cargoes which should help support supply and keep prices from increasing too quickly.

MOP prices are firm with very little downside. While MOP remains the most affordable raw material as it is the least supply constrained. Strong CPO/Oil Palm FFB prices have been strong in the quarter which should keep MOP demand strong.